by Blucer W. Rajaguguk, I Gusti Bagus Tridarwata Yatnaputra and Adrianus Paulus The Audit Board of the Republic of Indonesia (BPK)

Supreme Audit Institutions (SAIs) are invaluable in implementing the Sustainable Development Goals (SDGs), a set of 17 global goals with 169 targets to be accomplished by 2030. The United Nations (UN) believes SAIs are essential in promoting and fostering the efficiency, accountability, effectiveness and transparency of public administration.

The International Organization of Supreme Audit Institutions (INTOSAI) has set out to develop a framework for SDG-related audits. Because SDGs are global agendas, now, more than ever, coordination between SAIs in an audit is imperative. This article explores how working together through the audit process, particularly for SDG-related audits, can lead to more effective results and provide the most value to citizens worldwide.

The Cooperative Audit

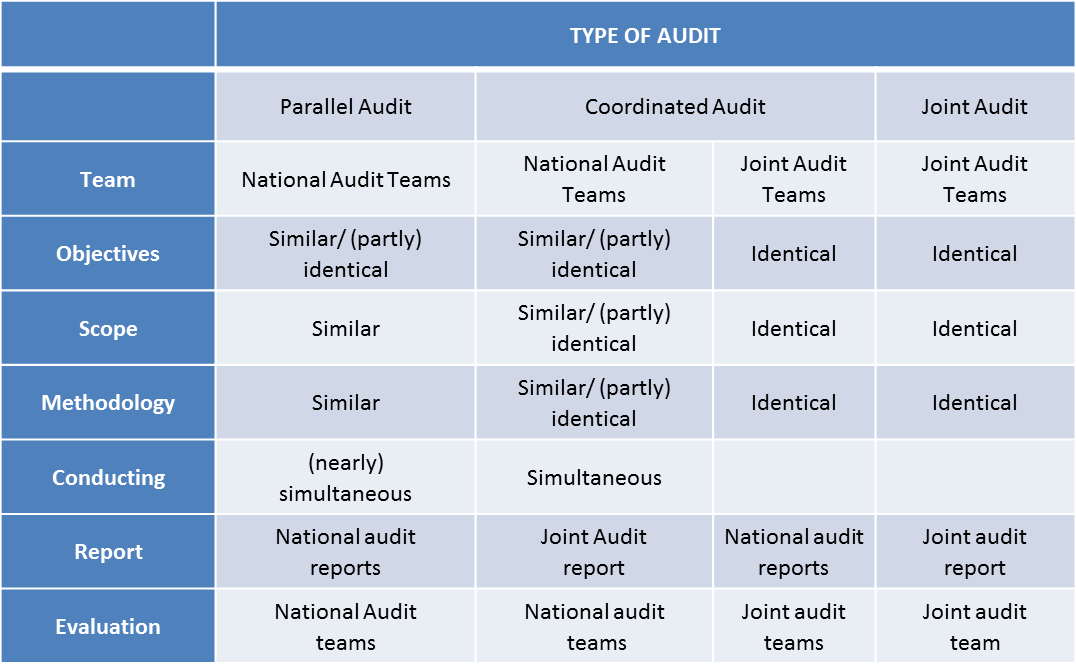

Cooperative audits (as outlined in the exposure draft of ISSAI 5800) are audits performed by two or more SAIs. There are three types of cooperative audits: parallel, coordinated and joint audit.

In a parallel audit, similar audits are conducted simultaneously by two or more auditing bodies. While each audit body has a separate audit team that reports to its own governing body on issues within its own mandate, both share the audit methodology and approach.

A coordinated audit is either a (1) joint audit with separate audit reports delivered to the individual SAI governing bodies or (2) parallel audit with a single audit report (in addition to separate national reports). In the joint audit, key decisions are shared, and the audit is conducted by one audit team composed of auditors from two or more autonomous auditing bodies who, usually, prepare a single joint audit report for presentation to each respective governing body (INTOSAI, n.d).

Table 1 outlines the characteristics associated with each type of cooperative audit; however, the distinction among the types is not always clear. According to the ISSAI 5800 exposure draft, the degree of cooperation “varies along a continuum from parallel audits to joint audits, and the type of cooperative audit chosen is not as important as is ensuring the SAIs holding the same opinion about all relevant points.”

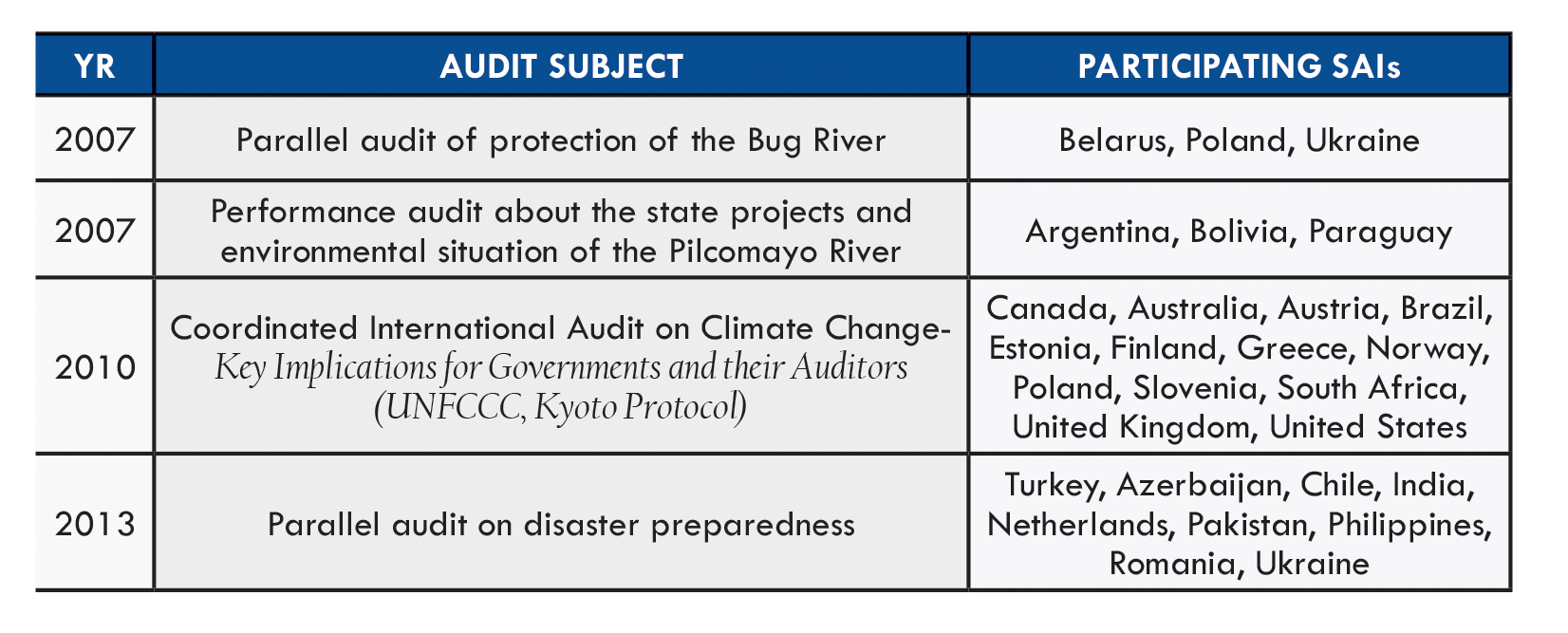

Cooperative audits have been conducted by SAIs in the past, particularly in the environmental arena (see Table 2). Cooperative audits enable SAIs to share audit standards, knowledge and experiences, and they provide a benchmark between SAIs, as well as between governments. Therefore, SDGs can be implemented evenly among countries, as countries are able to implement SDGs at the same phase and speed.

According to the 2015 Millennium Development Goals (SDG predecessor) report, global action is the only path to ensure that the development agenda leaves no one behind (United Nations, 2015). Cooperative audits are one such way to promote global actions in achieving SDGs and ensuring no one is left behind.

Is There A Best Type of Audit?

Compliance and performance audits are the most common types of cooperative audit to use on SDGs. Compliance audits are best in situations where SDGs are either partially embedded in a government’s programs or not embedded at all. In these environments, some existing government policies may have complied with SDGs (though not officially stated) while others might not.

Although SDGs are not legally binding, governments are expected to (1) adopt and establish national frameworks to achieve SDGs, (2) review the implementation progress using reliable data collection and analysis at the national level, and (3) contribute to the review at the regional and global levels (International Council for Science and International Social Science Council 2015, cited in Simpson 2016, p. 116).

In light of these expectations, the compliance audit objective is to assess the extent to which a country’s policies are compliant with the goals, targets and indicators at the national level. A cooperative compliance audit can also be conducted to review the compliance at regional and global level.

The Performance Audit Approach

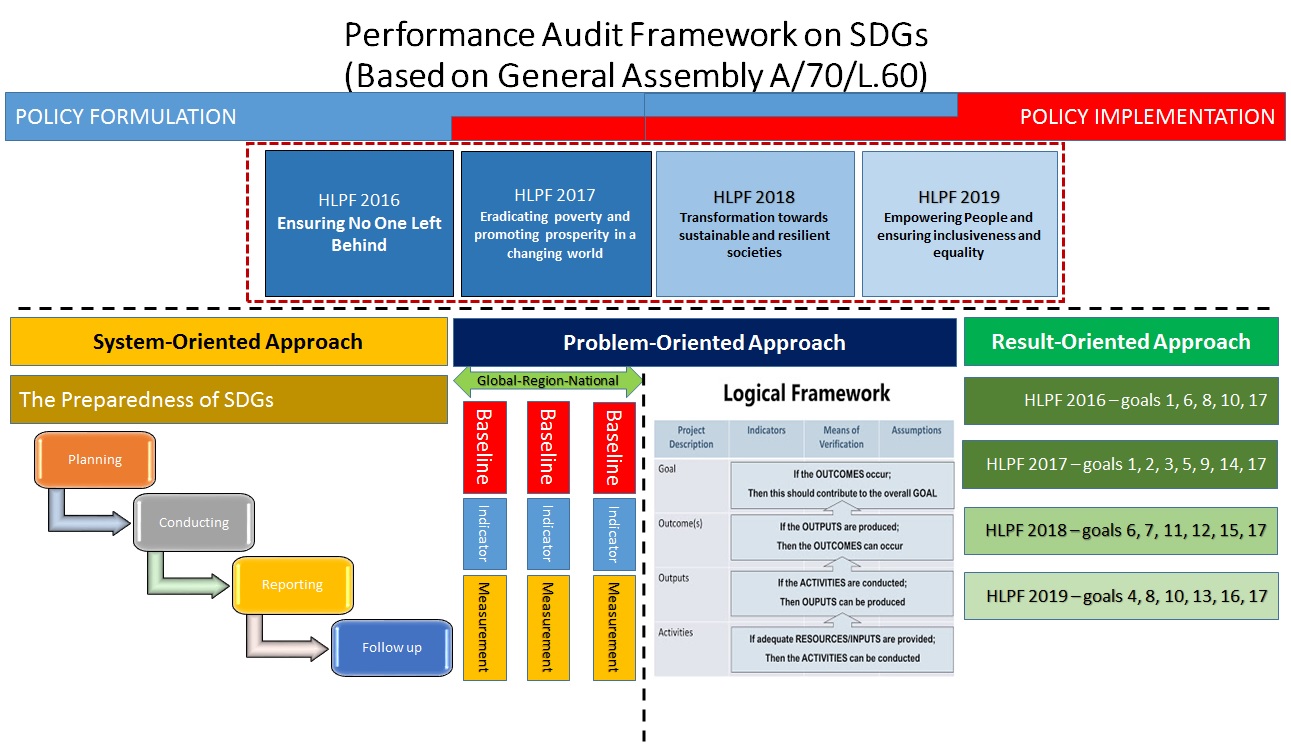

Performance auditing generally follows one of three approaches: system-, results-, and problem-oriented approach. An approach is selected based on the conditions and stage of implementation in each country.

The system-oriented approach is suitable for assessing national preparedness (or policy formulation), which included various activities associated with planning, conducting, reporting and follow up.

A results-oriented approach is suitable for the implementation phase, characterized by the exercising of deviations between fact and criteria (target). The system-oriented approach includes the planning, conducting, reporting, and follow-up processes. Planning refers to the incorporation of the Agenda into the national framework, such as national development plan, regulation and policies. Conducting refers to the availability of means of implementation, such as responsible bodies, prioritized target, and relevant data for performance measurement. Reporting refers to the availability of reporting mechanism and responsible bodies to collect the report. Follow up relates to an adjustment mechanism to use the monitoring report as an evaluation tool to improve the program in the future.

Problem-oriented approaches can be used in conditions where there is a high familiarity with implementing SDGs, which is often the case in most developed countries. Yet, the selected approach should also consider the availability of indicators. The challenge of sustainable development requires consistent, standardized and objective information that is timely and publicly accessible at no cost to end users. The United Nations Economic and Social Council (ECOSOC) has already established general indicators, and each country may have specific indicators previously developed. Auditors need to review the applicability of indicators to assist SAIs in audit result aggregation, both in the domestic and international framework.

Indonesia’s Experience During Implementation

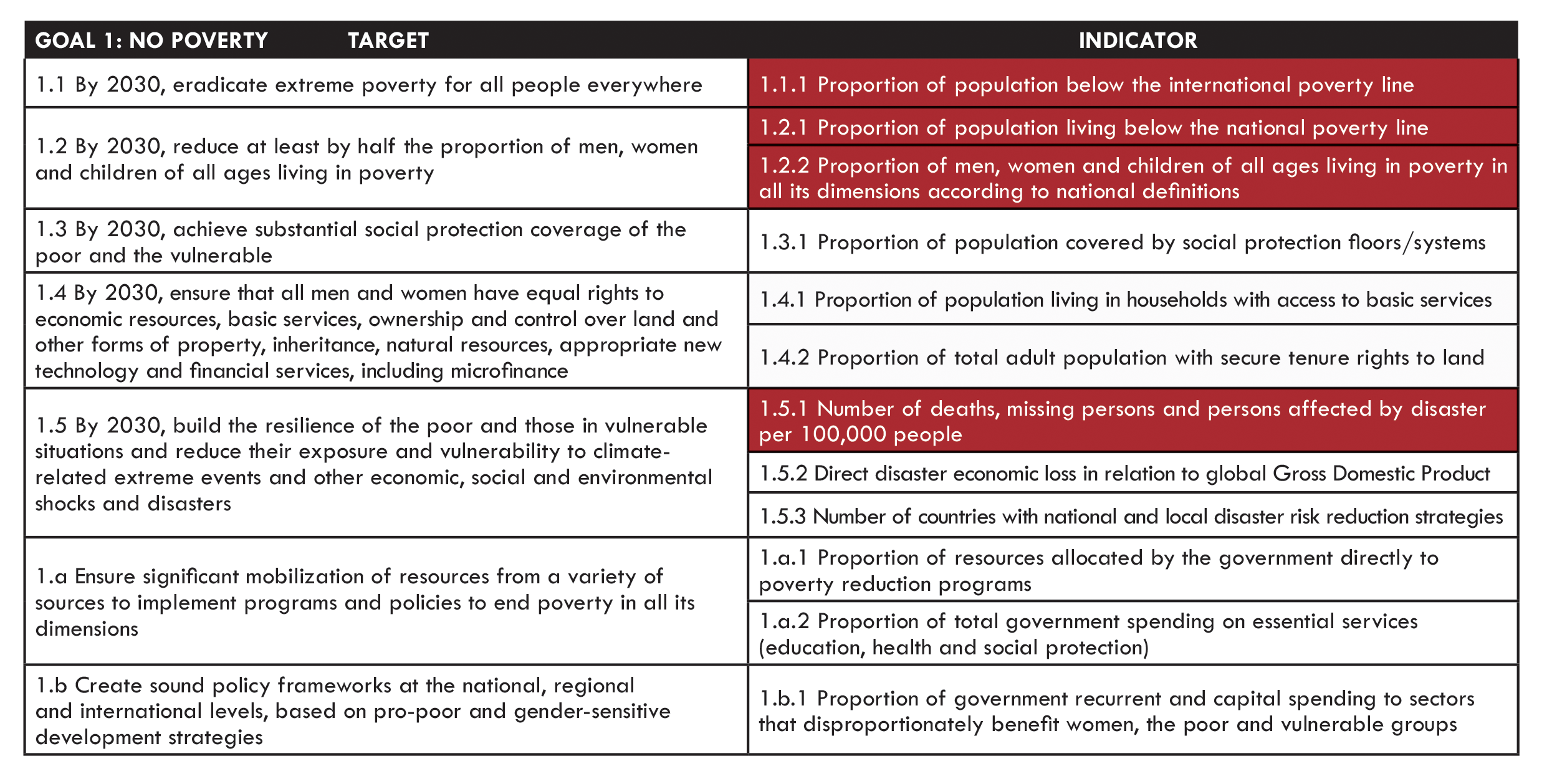

In the future, SAIs could design an appropriate audit based on indicator mapping. The United Nations has developed tables that illustrate targets and their associated indicators.

Specifically for Goal One (see Table 3), the alphabetical target listed at the end refers to the means of implementation necessary for the numerical target to be well-achieved. Indicators shown in the red area refer to available indicators in Indonesia.

Because audits on SDGs can be focused on specific targets or indicators, in the implementation phase SAIs can audit accomplishments of a single indicator or all available indicators associated with a target.

However, the data for some indicators are owned by several ministries, not solely the Bureau of Statistics. For example, nearly all of the Goal One data belongs to the Ministry of Agriculture, which requires SAIs to address the data’s validity.

Several questions are brought to light in these circumstances, such as “Does the Ministry of Agriculture have the authority and required resources to conduct data collection and computation? Is the data collected using accepted tools and methodologies?” Similarly, questions may also be raised for ECOSOC’s list of indicators that are not available locally, including, “Should SAIs encourage the government (in this case, the Bureau of Statistics) to start collecting those indicators?”

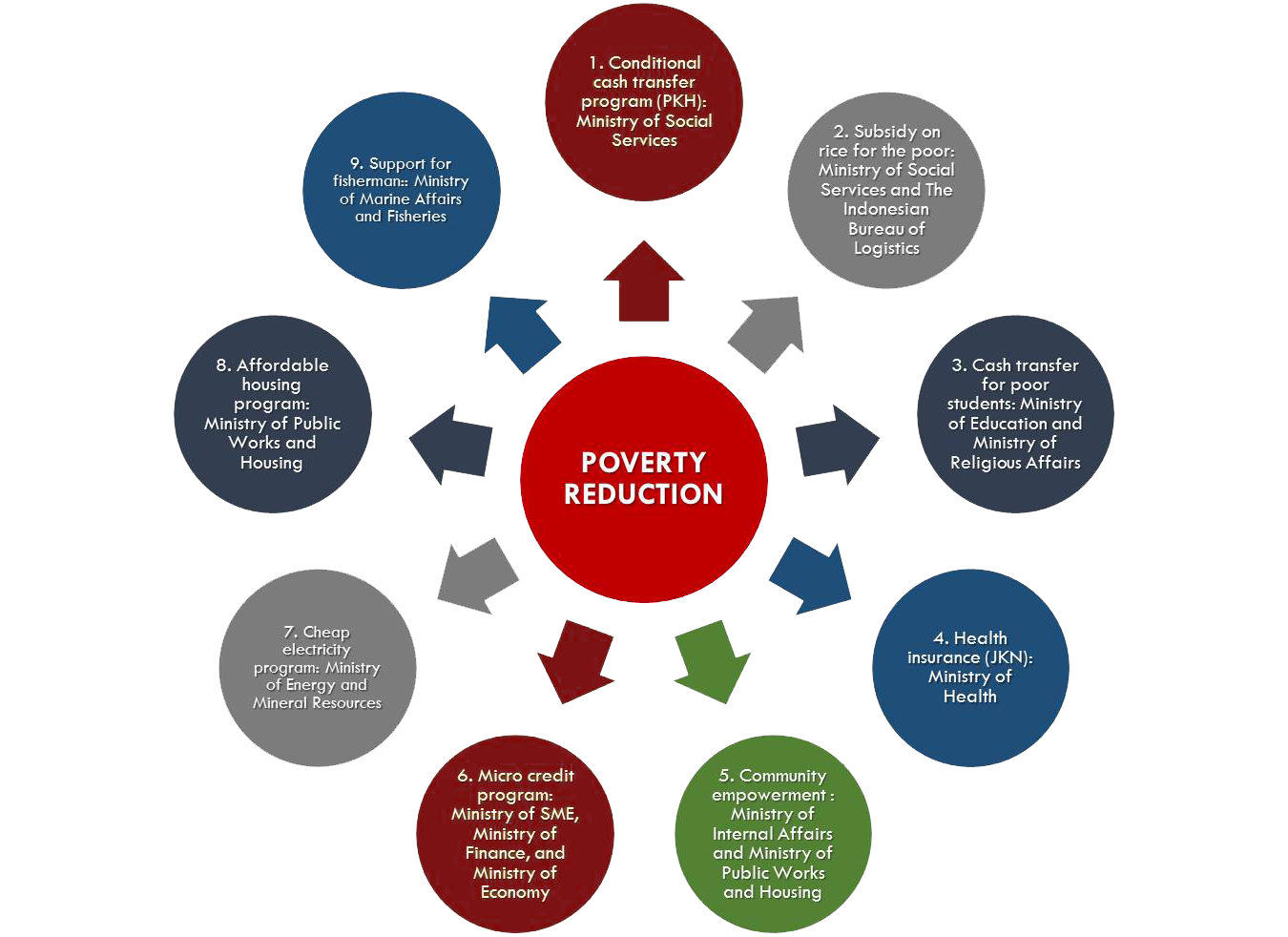

Coordinated Team Audits on Poverty Reduction Program—a case study

The poverty reduction strategy in Indonesia is complicated, as it involves nine programs delivered by a state-owned enterprise and eleven ministries (Figure 2). Despite these various programs, the poverty reduction target 2010-2014 was not accomplished. Not achieving the desired target motivated BPK to conduct a performance audit.

BPK configured a coordinated audit between BPK’s central and representative offices in several provinces. There are 12 audit teams from the central office to audit 12 government entities and 15 teams from each representative office that audit 15 provincial governments. Auditing provincial government is required to assess convergence between national and local strategy on poverty reduction. The audit resulted in a national (consolidated) report, as well as audit reports for each government entity.

Conclusion

Cooperative audits among INTOSAI members are crucial in sharing knowledge among SAIs, thus extending audit impact. Cooperative audits—parallel, coordinated, and joint—can be used to assess government preparedness and SDG implementation.

Compliance and performance audits can be utilized for SDG cooperative audits with the compliance audit being geared more so to a government that has not fully embedded SDGs into its program, yet. Regardless of the type of cooperative audit selected, collaborating on audits, sharing knowledge, experiences and best practices can help overcome obstacles, capitalize on opportunities, and, ultimately, better results for all stakeholders, particularly the citizens of the world.

For more information about this article and a full list of references, please contact Adrianus.Paulus@bpk.go.id.