Challenges in Transparency, Oversight as Governments Respond to Pandemic

by Claire Schouten, Senior Program Officer, International Budget Partnership, cschouten@internationalbudget.org

Amid a global pandemic that is forcing governments around the world to launch new spending measures, the International Budget Partnership’s (IBP) latest Open Budget Survey (OBS) shows why there is reason for concern: four out of five of the 117 governments assessed failed to reach the minimum threshold for adequate budget transparency and oversight under international standards.

Too often, governments fail to publish key budget documents that would clearly explain budget policies, decisions and outcomes, according to the new report. Worldwide, one-third of these important budget documents are not made available to the public. Among the notable missing items: 33% of the countries surveyed do not publish an annual Audit Report online in a timely manner.

Ongoing research by IBP and other organizations demonstrates an open budget process—one that is transparent, inclusive and accountable—offers a promising pathway for countries to thrive socially and economically.

While the 2019 OBS was completed just before the pandemic hit, it provides a telling snapshot of current government practices related to budget disclosure, opportunities for public engagement and effective checks and balances. Components and results of the survey include:

Budget transparency is assessed by public availability and contents of key budget documents all governments are expected to publish per international standards—specifically examining whether these key documents are comprehensive and published online in a timely manner.

The global average transparency score was 45 out of 100, short of the 61 considered the minimum threshold to foster an informed public debate.

Thirty-one governments scored 61 or higher, showing the goal is reachable by a range of government types. For example, Guatemala, Indonesia, the Kyrgyz Republic and Ukraine all reached or surpassed a score of 61 within the last two OBS rounds.

Examples of strong budget transparency are found in six of the seven regions of the world.

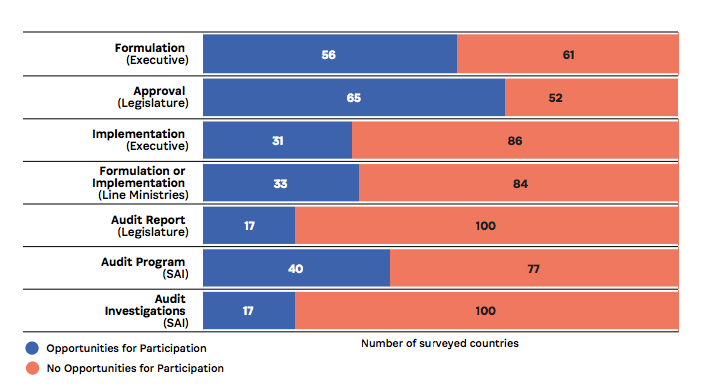

Public participation, assessed based on formal opportunities for civic organizations and individuals to engage and provide input throughout the budget process, had a dismal average global score: 14 out of 100. The OBS looks for seven different types of participation mechanisms in three government bodies, namely the executive, legislative and Supreme Audit Institution (SAI). Examples include public consultations, pre-budget submissions, participatory budgeting, advisory councils and social audits.

Four out of five countries have at least one mechanism for engaging the public at some point during the budget process; however, 24 countries have no opportunities at all. Eleven nations in OBS 2019 have five or more different public engagement mechanisms. Only three—New Zealand, South Korea, and United Kingdom—have opportunities for public engagement in each of the seven types of mechanisms.

In the audit process, public participation opportunities are most common during the audit program planning phase. SAIs in 40 countries have some mechanism for public input to the audit plan, but only 21 SAIs provide feedback on how this input was used. Levels of public engagement with the auditor in this survey round were largely the same as in the previous one completed in 2017, which showed public participation with the auditor is strong in Latin America, especially in shaping the audit plan (15 of the 18 countries assessed in the region have a mechanism to seek public input).

OBS 2019 finds public engagement is especially lacking during the budget implementation and oversight phases. More governments engage with the public when formulating or approving the budget (see Figure 1).

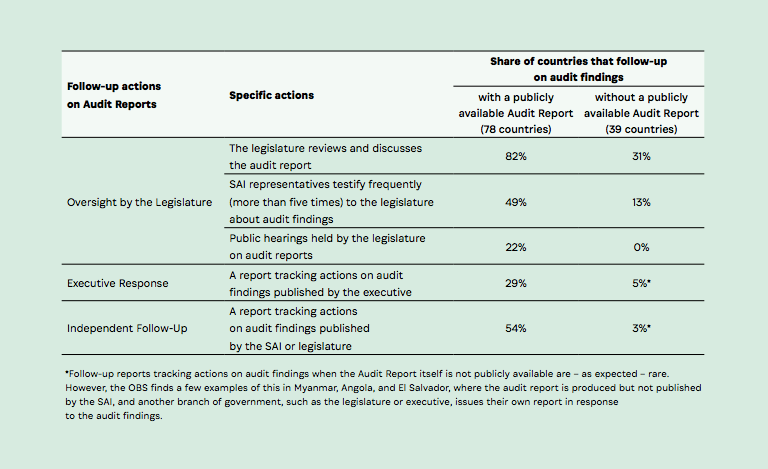

Oversight is measured based on roles played by legislatures and SAIs in the budget process, with 61 out of 100 considered an adequate score. Of the 117 countries surveyed, 34 have adequate oversight from legislature, 71 from the SAI and only 30 from both institutions.

Key follow-up from the legislature or executive is often lacking (see Figure 2). Most countries with a publicly available Audit Report have a legislative committee review the report and half have a SAI representative frequently testify on audit findings to the legislature. On the other hand, less than one-third of the governments’ executives publish a report responding to the audit findings. Only 17 countries with a publicly available Audit Report also have public hearings of the legislature on the audit findings.

Nearly all countries are missing at least one follow-up action, and only six have all five legislative and executive follow-up actions: Australia, Canada, Georgia, New Zealand, Norway, and Peru.

Open budget systems alone cannot solve the pandemic, but they can strengthen the bonds between people and government and improve public service delivery. It will take a concerted effort across all stakeholders to ensure governments provide sufficient levels of public fund transparency and accountability to contribute toward the Sustainable Development Goals and the Paris Climate Agreement, let alone ensure countries have the oversight systems to tackle the next crisis. For this reason, IBP launched a call to action to galvanize civic actors, businesses, donors and governments to work together to accelerate progress on open budgets.

The INTOSAI Development Initiative (IDI) has joined IBP and organizations from more than 100 countries on this call to action. Together with SAIs, civil society organizations and international bodies, such as the German Development Cooperation and United Nations Department of Economic and Social Affairs, we are collaborating to further strengthen audit accountability and impact by enhancing SAI-civil society cooperation and citizen engagement.

IDI and IBP will release a report later this year that delves more deeply into the OBS findings and on the value of audit and oversight in the accountability ecosystem and development agenda. We look forward to engaging further with the public audit community to ensure informed, inclusive and accountable public financial management and benefits for all.

The Open Budget Survey is part of the International Budget Partnership’s Open Budget Initiative, a global research and advocacy program to promote public access to budget information and the adoption of inclusive and accountable budget systems.